OK … regular readers will recall that my view of the current single-family home (SFH) investment climate presents a once-in-decades windfall for savvy SFH landlords wanting to increase their portfolio of rental units. Likewise, those considering a “toe-in-the-water” initiation to the world of rental real estate investing will do well to recognize that now is a good time to save money and build equity!

Read on and then request your FREE personalized Wealth Creation analysis.

While my crystal ball may be cloudy from time-to-time, I’m feeling confident that the opportunity to capitalize on the “perfect storm” of low interest rates and anticipated inflation more than offset any increased prices for SFHs in this low-inventory market. Here’s why.

Low Interest Rates

Uncertainty strikes fear into the heart of every investor. When it comes to interest rates it’s is a safe-bet that they will remain low for the foreseeable future. No less an authority than Federal Reserve Chairman Jerome Powell has said interest rates will remain at or near zero through 2023. That underscores the Fed’s intention to keep longer-term (read residential mortgage rates) interest rates low … currently in the 2-3 percent range.

That’s good news for SFH investors as lower interest rates help qualify borrowers for the purchase of homes that have increased in sales price. Today’s interest environment is a perfect invitation to lock in 30-year fixed rate financing. Now, factor in the effect of inflation on the significant boost in leverage SFH landlords will enjoy when inflation is ladled into the equation. In short …

- Borrowing at interest rates less than inflation = leverage

- Borrower’s interest rate minus the rate of inflation = real interest rate

To clarify with an example … a loan with a 5 percent nominal rate when offset by an inflation rate of 3 percent means the borrower’s out-of-pocket interest cost is 2 percent.

For a full discussion of this financial phenomenon, be sure to invest less than 4 minutes to read our January article … When Inflation Is Your Friend … Borrowing Converts Cost to Profit.

The Case to Anticipate Inflation – Increasing Wage Pressure

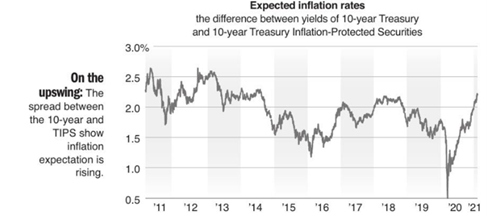

Inflation is a measure of the rate of rising prices of goods and services in an economy. Borrowers win with inflation … lenders are paid back with money that is worth less than when it was originally borrowed. Inflation is a function of a rise in prices due to increases in production costs … wage hikes are a major factor.

So, a word about Virginia wage hikes … anticipated and real.

Beginning May 1, 2021, the Virginia hourly minimum wage will initiate a step-rate schedule of implementation. The revised roll-out starts May 1, 2021 at a minimum hourly wage of $9.50 and escalates to $15.00 mid-summer 2024 … subject to General Assembly action.

The American Rescue Plan Act of 2021 extends federal unemployment compensation through the week ending September 4, 2021. Qualified claimants will receive $300 per week in addition to Virginia unemployment compensation.

Now let’s put that in perspective for both workers and employers. The maximum Virginia weekly unemployment benefit is $378 for no more than 26 weeks … the minimum is $60. Assuming a start-date of April 1, 2021, Virginia benefits expire 3 weeks after the current federal extension of benefits.

So, effective May 1, 2021, the Virginia mandated minimum hourly wage is $9.50. Assuming a 40-hour work week, that is comparable to a minimum combined federal and state hourly payment of $9.00 … not subject to income tax! ($360 divided by 40 hours = $9.00).

At the top-end of Virginia unemployment compensation of $378, there is a dramatic difference in the effective non-taxable hourly rate … $16.95! ($678 divided by 40 hours = $16.95) What does that mean? I anticipate the potential for 4 consequences:

- There is motivation for many workers to stay on the sidelines until the end of September.

- Employers will need to pay a premium over current wages to retain and attract quality talent as the post-Covid economy builds steam.

- Post-pandemic workers will have a magnified mind-set in their compensation demands.

- In the wake of C-19, pent-up demand for pandemic-deprived products and services will propel more consumer spending that will drive prices in an upward trajectory.

Net effect on inflation … mounting pressure!

The Case to Anticipate Inflation – Federal Stimulus & Government Spending

Expectations for inflation are increasing. Many in the financial markets express concern that the more than $4 trillion in support provided by Congress last year coupled with the most recent $1.9 trillion C-19 relief measure could ignite inflation. As further evidence of concern, there is talk among White House insiders that President Biden will be presented with a $3 trillion infrastructure and jobs package.

House Minority Leader Mitch McConnell says unfunded spending of that magnitude would “unleash inflation”.

Two additional items are worth noting. Biden campaigned on raising corporate tax rate from 21% to 28% … increases likely to be passed on in higher consumer prices. Additionally, Covid-19 vaccines apparently are bringing daily life closer to normal which leads many observers preparing for price increases across the economy.

Click here to learn more about the synergy of Interest, Inflation and SFH Inventory.

Key Takeaways

Yes, I agree that bargains on single family home purchases are scarce. That said, there is significant upside cash-flow and asset growth potential given the synergy of super-low interest and likely prospects for inflation … a one-two-punch that minimizes the net effect for investors given today’s higher home sale prices.

While inventory remains low … there are SFHs for sale, albeit they are swept off the market in lightening-like speed. So, align yourself with a lender and real estate professional who will be alert and promptly present opportunities to you for your purchase consideration.

There is a sense of urgency for SFH investors. This week Chairman Powell told congress that as the pandemic fades and the economy opens, the Fed expects inflation will rise over the course of this year. He said that if inflation did start to increase in worrisome ways, the Fed could keep it under control by raising interest rates. While that’s not a reversal of his earlier position that interest rates will remain at or near zero through 2023, it does say that SFH investors’ boost in leverage … historically low interest rates in a climate of increasing inflation … may be short-lived.

FREE Personalized Wealth Creation Analysis

Request your FREE Wealth Creation Analysis and Learn How You Can Increase the Value of Your Residential Rental Portfolio … or Become a First-time Landlord.

Call or email Bill Le to schedule your brief, confidential telephone session. You’ll find your 10-minute investment of time well worth it … plus receive a comprehensive print-out of the benefits to you based on the sample purchase info you share.

E: ble@krsholdings, or

DD: 804-376-8471