The 3 R’s of the Economy: Recession, Recovery, Recession

By Kyle Stephenson Thursday, March 21, 2019

Where Are We Now … What’s on the Horizon

Generally, I’m pleased with my projections for the economy over the last several years … especially as it has impacted residential real estate investors and tenants. Now, I offer a note of caution as I envision embryonic, yet clearly evident, signs that the market is slowing. In my mind, there is unmistakable evidence that recession is looming as we approach the end of the peak economic cycle we’ve enjoyed these past nine years or so.

Admittedly, while I am firmly convinced that the downturn will come, my crystal ball does appear a bit cloudy as to when. That said the following article will offer some indications that several trends are afoot that quite often are 2-year precursors to a financial slump.

A Bit of History – Recessions > Recoveries > Recessions

As you are reading this, the U.S. will have experienced the third longest period of economic expansion following a recession. In this case, it is particularly dramatic for two reasons:

The Great Recession of 2007 – 2009 was the worst business contraction since WW II.

If the expansion continues to perk along, it will break an all-time record of 120 months at the end of June of this year.

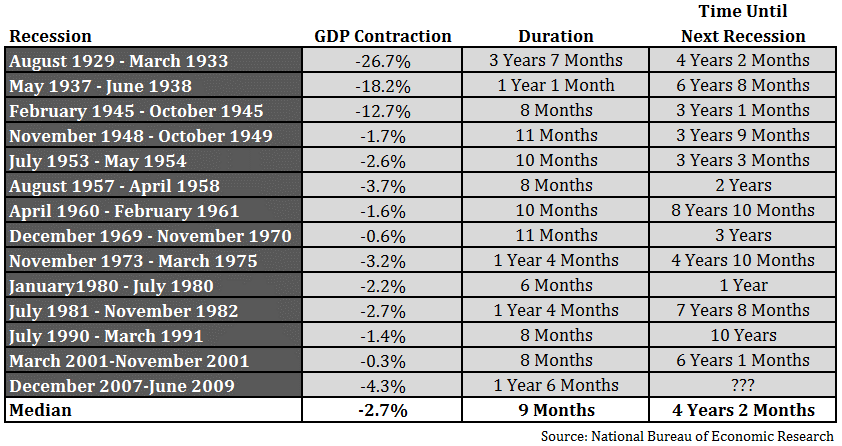

Interestingly, as severe as it was, the Great Recession pales in comparison to recessions in the early 20th century. Take a look at the effects of every recession since the Great Depression in 1929.

It’s now over 9 years since the end of the Great Recession. While the median time between recessions is a little over 4 years, we may see a 10 year run in this recovery … or longer. Of course, as the chart above illustrates, there is no set timetable for recessions or recovery times. But there is one thing you can count on, business cycles are a reality and “all good things economy-wise” will come to an end.

What to Expect … What to Look For

Many experts point to the extended recovery time record due to the Federal Reserve exercising an accommodating, super-cautious approach to Fed interest rate hikes. Since WW II, the Fed responded to recessions with a series of interest rate hikes.

In contrast, the U.S. central bank kept its benchmark short-term interest rate near zero until recently and then only with disciplined increases. By one report, even the most hawkish committee members anticipate interest rates to remain at historic low levels for years to come.

Four Items to Watch with Measured Concern

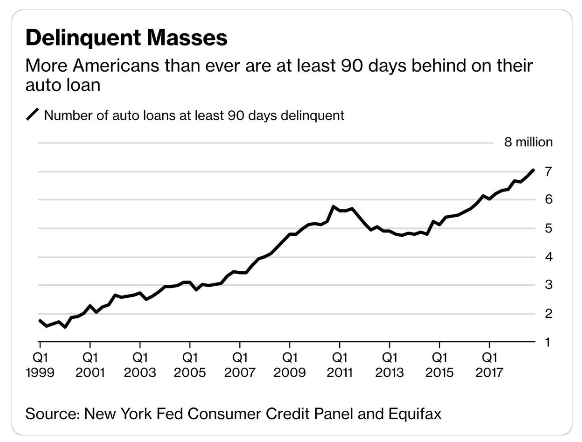

Delinquent Car Loans

The Federal Reserve Bank of New York reports at least seven million American consumers were seriously late on auto loans at the end of last year. Notably, most of which are Millennials. In 2018, auto debt accounted for about 9 percent of total U.S. consumer debt, up from 6 percent in late 2011… a 50% jump.

In contrast, that’s one million more delinquencies than at the end of the Great Recession.

The report found that a majority of the borrowers who were behind on car payments were under the age of 30. This makes sense since Millennials and Generation Z are the ones who are already straddled with budget-crushing student loan payments. Add a crippling car payment and it is a recipe for financial calamity.

So given a young borrowing population, unemployment at four percent and job openings at an all-time high, may prompt incurring car loans for a coveted new vehicle while ignoring the fiscal consequences if it ends up they can’t afford the “ride”.

Home Mortgage Loan Delinquencies

No less an authority than Moody’s reports that mortgage delinquencies are on the rise. The drivers seem to be twofold:

Loosened underwriting standards by lenders, and

Slowing home price growth (more on that in a moment)

Residential loan originators are pressed to produce volume in loan originations. Interest rates are up and refinancing volumes have greatly declined so it follows that underwriting standards for purchase loans will be liberalized to attract new home buyers.

Of course, this can put consumers at risk if this accommodating lending environment leads to incurring more debt than can be serviced in the event of even a minor economic turnaround.

Slowing Home Price Growth

Nationally, the median sales price of single family homes has slowed … and in some U.S. communities has become stagnant or even cratered. According to Redfin, the National median sale price for single family homes was $287,400 in 2018 … a mere growth rate year-over-year of 0.6%.

To put that in perspective for Central Virginia, that rate of price braking has not yet been realized. Notably, Richmond median sale prices last year were at $232,200 … featuring a growth rate of 2.5% over the prior year. The Hampton Roads markets clocked in at $220,000 with a growth rate of 1%.

So will Central Virginia drift toward the growing home price malaise increasingly realized nationally? No way to predict, but worth staying alert to developments.

Rising Rents

According to last month’s Zillow Real Estate Market Report rent prices grew at their fastest rate in 10 months yielding year-over-year appreciation of 2.4%. This rise means more than a $400 annual bump in housing expense for the typical renter

The upshot for both landlords and tenants is the reality that rent increases cannot grow faster than income over the long term. That fact fuels the expectation that a slow-growth rental market is on the horizon. A further driver is the projected softening in demand for rentals as many Millennials opt for home ownership.

Summary

So it’s not a matter of “if” … it’s a matter of “when” the next phase of the recurring business cycle will surface. The current upswing, while impressive, has gone on long enough to lull some people into a false sense of complacency. Without a doubt, it is a time to hope for the best and plan for the worst. To do otherwise puts landlords, business owners, managers and investors at considerable risk.

Be sure to watch for April’s article to learn 6 things you can do to thrive when the recession surfaces. back

Generally, I’m pleased with my projections for the economy over the last several years … especially as it has impacted residential real estate investors and tenants. Now, I offer a note of caution as I envision embryonic, yet clearly evident, signs that the market is slowing. In my mind, there is unmistakable evidence that recession is looming as we approach the end of the peak economic cycle we’ve enjoyed these past nine years or so.

Admittedly, while I am firmly convinced that the downturn will come, my crystal ball does appear a bit cloudy as to when. That said the following article will offer some indications that several trends are afoot that quite often are 2-year precursors to a financial slump.

Generally, I’m pleased with my projections for the economy over the last several years … especially as it has impacted residential real estate investors and tenants. Now, I offer a note of caution as I envision embryonic, yet clearly evident, signs that the market is slowing. In my mind, there is unmistakable evidence that recession is looming as we approach the end of the peak economic cycle we’ve enjoyed these past nine years or so.

Admittedly, while I am firmly convinced that the downturn will come, my crystal ball does appear a bit cloudy as to when. That said the following article will offer some indications that several trends are afoot that quite often are 2-year precursors to a financial slump.

It’s now over 9 years since the end of the Great Recession. While the median time between recessions is a little over 4 years, we may see a 10 year run in this recovery … or longer. Of course, as the chart above illustrates, there is no set timetable for recessions or recovery times. But there is one thing you can count on, business cycles are a reality and “all good things economy-wise” will come to an end.

It’s now over 9 years since the end of the Great Recession. While the median time between recessions is a little over 4 years, we may see a 10 year run in this recovery … or longer. Of course, as the chart above illustrates, there is no set timetable for recessions or recovery times. But there is one thing you can count on, business cycles are a reality and “all good things economy-wise” will come to an end.

The report found that a majority of the borrowers who were behind on car payments were under the age of 30. This makes sense since Millennials and Generation Z are the ones who are already straddled with budget-crushing student loan payments. Add a crippling car payment and it is a recipe for financial calamity.

So given a young borrowing population, unemployment at four percent and job openings at an all-time high, may prompt incurring car loans for a coveted new vehicle while ignoring the fiscal consequences if it ends up they can’t afford the “ride”.

Home Mortgage Loan Delinquencies

No less an authority than Moody’s reports that mortgage delinquencies are on the rise. The drivers seem to be twofold:

The report found that a majority of the borrowers who were behind on car payments were under the age of 30. This makes sense since Millennials and Generation Z are the ones who are already straddled with budget-crushing student loan payments. Add a crippling car payment and it is a recipe for financial calamity.

So given a young borrowing population, unemployment at four percent and job openings at an all-time high, may prompt incurring car loans for a coveted new vehicle while ignoring the fiscal consequences if it ends up they can’t afford the “ride”.

Home Mortgage Loan Delinquencies

No less an authority than Moody’s reports that mortgage delinquencies are on the rise. The drivers seem to be twofold: